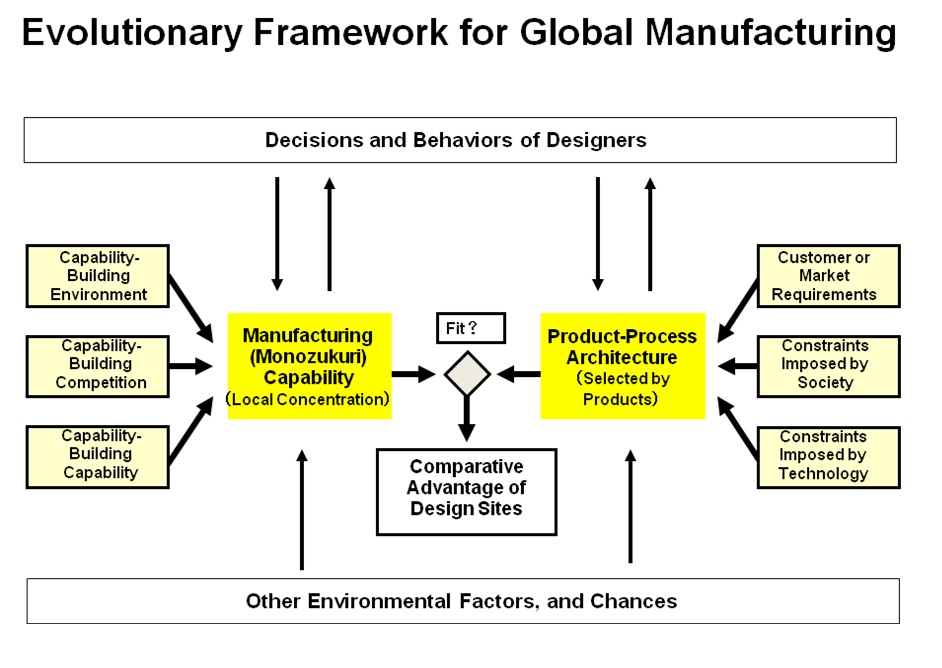

Takahiro FUJIMOTOTHE FUTURE OF THE JAPANESE INDUSTRIES: AN APPROACH IN TERM OF DESIGN-BASED COMPARATIVE ADVANTAGE Takahiro FUJIMOTO Professor, Faculty of Economics, MMRC, University of Tokyo  The US financial crisis hit Toyota and other Japanese firms that depended heavily on the US economic-bubble-driven exports, and yen was appreciated during the same period. Many Japanese factories continued to move to low cost countries like China. Some of large firms in lower cost countries such as Korea started to outperform Japanese counterparts. – These facts and concerns lead to spread of various types of industrial pessimism: Many observers in and out of Japan started to argue that this is the beginning of “the end of Japanese manufacturing.” On the other hand, however, Japanese export activities remained fairly high after the crisis – 50 trillion yen or over 10% of its stagnant GDP, with over 6 trillion yen of trade surplus in fiscal year 2009. There are still many Japanese firms with record high profits and continued growth. Note that, while media tend to focus on the hardship of bad performers, better performers (smaller ones in particular) are generally silent, as they do not want to become targets for price-cutting pressures. This indicate that the reality of Japanese economy is a more mixed one than an “all-dark” view that the media tend to advocate. In fact, if we can still predict the global expansion of free trade as a long-term trend in the 21st century, and if we also believe in David Ricardo’s theory of international division of labor based on comparative advantage as an economic wisdom from the 19th century, it should be common sense that industrialized countries have, after all, something to export and other things to import. It is neither meaningful nor constructive to ask whether Japanese manufacturing sector is totally hollowed out. The realistic question should be (i) in what areas Japanese manufacturing sites maintain comparative advantage, (ii) and what levels of relative wage, living standards, and exchange rate are compatible with its trade balance. Since today’s major firms extend their activities across borders, these questions are translated into where to design, produce, and sell their products on a global scale. The author’s tentative answers to these two questions are as follows (see also Figure): (i) a dynamic fit between products’ architecture and sites’ capability affect the comparative advantage of the goods and sites in question; (ii) capability-building competition among the competing manufacturing sites affects relative wage levels that are compatible with balanced trade. We call this framework design-based view of comparative advantage, which may provide us with additional explanation to today’s trade phenomenon (e.g., intra-industrial trade), alternative classification of industries, and a calmer approach to the problem of industrial hollowing out. The evolutionary framework of architecture-based comparative advantage leads to a hypothesis that dynamic fit between organizational capability and product-process architecture tends to result in complicated patterns of international division of labor. While most existing trade theories focus on the question of “where to produce,” this approach starts from a simple fact that a design process precedes a production process, and thus emphasize another important question – where to design. Because design of an artifact is nothing but coordination of its functional and structural elements prior to production, we should pay attention to coordinative aspects of capability and architecture. A manufacturing site’s capability reflects the historical system evolution of a nation or region in question. In post-war Japan, for example, “economy of scarcity,” that is, chronic shortage of labor, material, and financial input caused by Japan’s rapid and continuous economic growth in the 1960s to 80s, through long-term employment and transactions for preserving such inputs, resulted in disproportionate accumulation of coordinative (integrative) capabilities in the country. And this coordination-rich capability of manufacturing sites, once established, became a source of competitive advantage in coordination-intensive products with complex and integral architecture. Thus, a prediction derived from this design-information-architecture view of industry is that Japanese firms and industries should base their strategies on its traditional strength; that is, coordinative-integrative organizational capability and coordination-intensive (i.e., complex-integral) products for the time being. More generally, each country should exploit its existing capability and architecture in the shorter run, while exploring its potentials in alternative types of capability and design in the longer run. Different countries and regions have different histories. And history matters as a basis of their competitive advantage. Industrial hollowing out may happen more often in the area where the capability and architecture do not fit, but compensating industrial development may be observed in the area where the dynamic fit is present – this is an insight derived from our design-based, or “monozukuri-based,” theory of trade and industries.  |

|

|

Recherche | |

FFJ Research Statement | |

Takahiro FUJIMOTO |

| Inscrivez-vous à notre Lettre en cliquant ici |

*En cas de problème, vous pouvez aussi vous inscrire en envoyant un mail à sympa@ehess.fr, avec pour titre "subscribe ffj_french_news".

| Contact | | Mentions légales | | © Copyright Fondation France-Japon de l'EHESS | | Réalisation Aneol |  |